CapEx vs OpEx Financial Strategy: A Director’s Guide to Capital Allocation

In corporate finance, mastering the CapEx vs OpEx financial strategy is the hallmark of a sophisticated leadership team. It is not merely an accounting classification; it is a strategic lever used to optimize tax efficiency, manage cash flow, and drive long-term business valuation.

1. Defining the Fundamentals of Spending

Every dollar exiting the business must be categorized as either an investment in future capacity or a cost of the present operations.

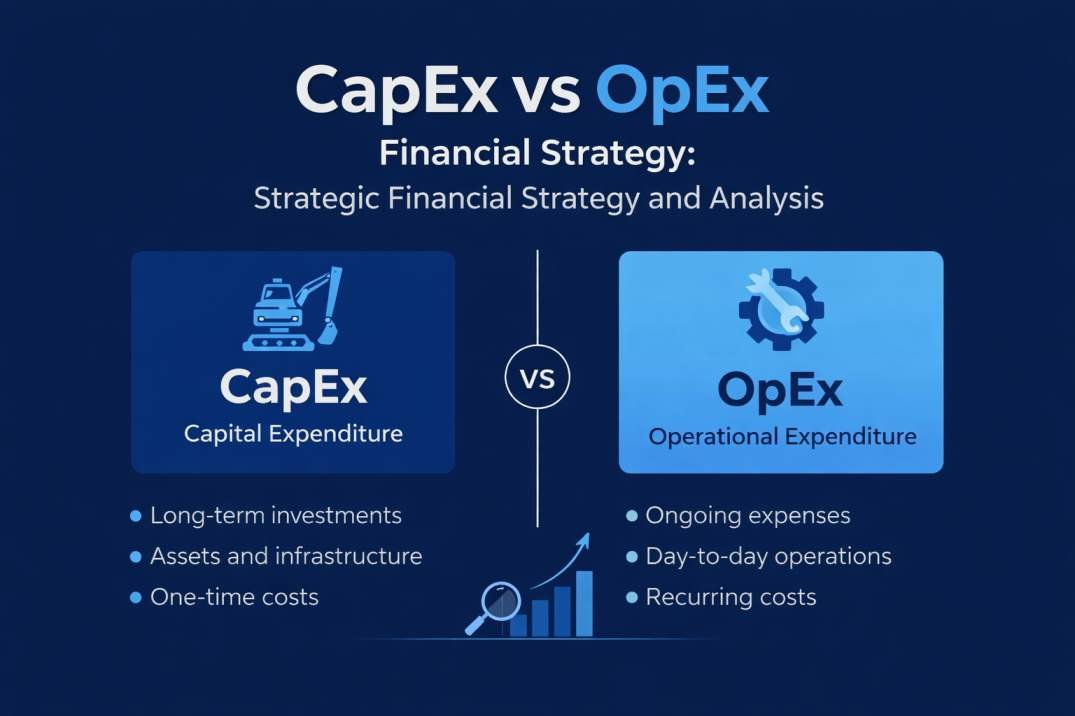

What is CapEx (Capital Expenditure)?

CapEx represents the acquisition of physical or intangible assets that provide value for more than one year. These are “capitalized” because they represent wealth that remains within the company, just in a different form.

- Core Examples: Real estate, industrial machinery, manufacturing robots, and capitalized software development.

- Financial Impact: Recorded as an asset on the Balance Sheet; expenses hit the P&L slowly over time through depreciation.

What is OpEx (Operating Expenditure)?

OpEx covers the day-to-day costs required to maintain the business. These expenses are fully consumed within the current accounting period.

- Core Examples: Salaries, office rent, SaaS subscriptions, utilities, and marketing.

- Financial Impact: Recorded immediately as an expense on the Income Statement (P&L).

2. CapEx vs OpEx Financial Strategy: Key Comparison

| Feature | CapEx Strategy | OpEx Strategy |

|---|---|---|

| Accounting | Capitalized; depreciated over years. | Fully expensed in the current period. |

| Tax Impact | Slow relief via depreciation. | Immediate 100% tax deduction. |

| Cash Flow | Large, upfront cash outflow. | Small, recurring payments. |

| Profit Impact | Does not lower EBITDA directly. | Lowers EBITDA immediately. |

3. Strategic Financial Formulas

To execute a successful CapEx vs OpEx financial strategy, we use these two primary formulas:

A. Straight-Line Depreciation Formula

Used to spread the cost of a CapEx asset over its useful life:

Annual Depreciation = (Cost of Asset – Salvage Value) / Useful Life

B. Net TCO (Total Cost of Ownership) Comparison

Used to decide between buying (CapEx) or leasing/subscribing (OpEx):

Net CapEx Cost = (Initial Investment + Maintenance) – Tax Shield from Depreciation

4. Real-World Case Study: The Logistics Fleet

A delivery firm requires 10 new vans to expand its route capacity. The choice between CapEx and OpEx changes the firm’s financial health profile:

Scenario A (CapEx Strategy): Buy for $500,000

The Balance Sheet grows by $500k in assets. Only $100k (depreciation) is deducted from profits annually. This strategy builds equity but drains immediate cash.

Scenario B (OpEx Strategy): Lease for $12,000/month

The full $144,000 annual lease is deducted from profits immediately. Cash is preserved for hiring, but the company owns no assets at the end of the term.

Board-Ready Business Case Template

Use this structure when presenting a CapEx vs OpEx financial strategy to your stakeholders or Board of Directors:

- Executive Summary: State the operational need and the two financial paths identified.

- Cash Flow Analysis: Compare the Year 0 “cash hit” of CapEx vs. the multi-year liquidity impact of OpEx.

- Tax Shield Projection: Calculate the immediate tax savings of OpEx vs. the long-term depreciation benefits of CapEx.

- EBITDA & Valuation Impact: Explain how CapEx preserves EBITDA for valuation purposes (e.g., if preparing for an exit).

- Risk Assessment: Address asset obsolescence (Risk of owning) vs. variable cost inflation (Risk of leasing).

- The Director’s Recommendation: Provide a clear choice based on the current Weighted Average Cost of Capital (WACC).