Managing Personal Finances: Complete Guide to Budgeting, Saving, Investing & Financial Stability

Managing personal finances is one of the most important life skills for achieving financial stability, reducing stress, and building long-term wealth. Without proper financial management, people often struggle with debt, poor budgeting, low savings, and financial insecurity.

Good financial management helps you:

- Control spending

- Reduce debt

- Build emergency savings

- Improve financial security

- Increase wealth over time

- Prepare for retirement

- Achieve personal financial goals

At Consultant4Companies, we help individuals and businesses improve budgeting, forecasting, cash flow management, and financial planning strategies.

Why Managing Personal Finances Matters?

Poor financial management creates stress, uncertainty, and long-term financial problems. Many people earn good incomes but still struggle financially because they lack budgeting discipline and financial planning.

Managing personal finances helps you:

- Track income and expenses

- Build savings

- Avoid unnecessary debt

- Improve cash flow

- Prepare for emergencies

- Grow investments

- Create long-term financial security

Financial discipline is not about becoming rich quickly. It is about making consistent smart decisions over time.

Read also:

Proactive Approach Mastery

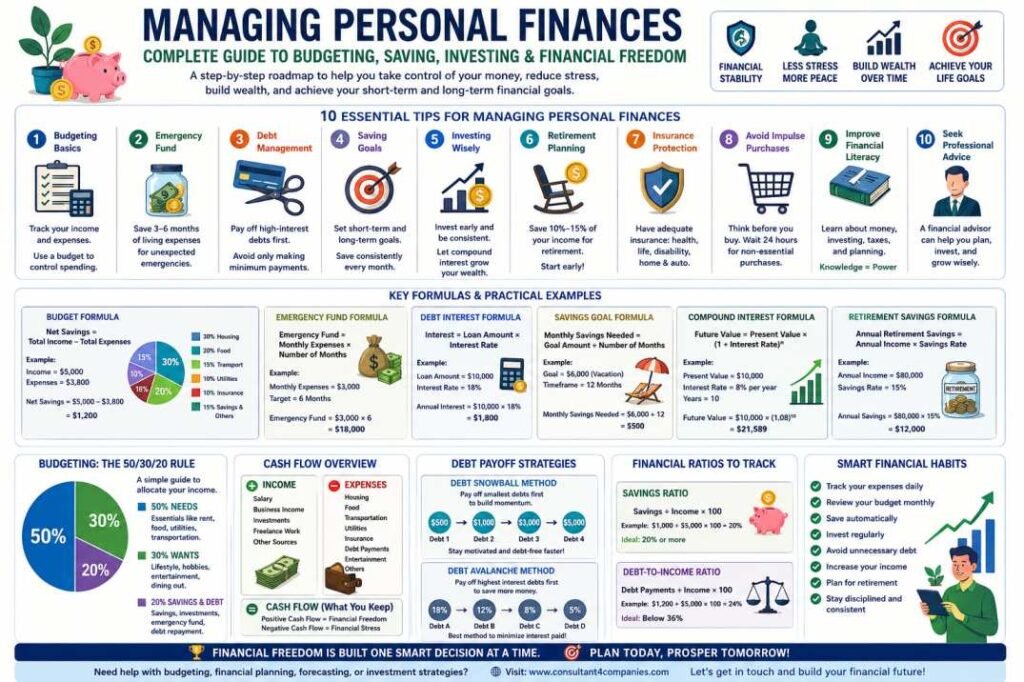

10 Essential Tips for Managing Personal Finances

Financial discipline is not about becoming rich quickly. It is about making consistent smart decisions over time. Here are the 10 essential tips:

1. Budgeting Basics

The first step in managing personal finances is creating a detailed budget.

A budget helps you understand:

- How much money you earn

- How much money you spend

- Where your money goes

- How much you can save

Monthly Budget Formula

Net Savings = Total Income – Total Expenses

Budget Example

- Monthly income = $5,000

- Monthly expenses = $3,800

Net Savings = $5,000 – $3,800 = $1,200

This means you save $1,200 every month.

You can use budgeting apps or spreadsheets to track spending categories like:

- Rent or mortgage

- Utilities

- Food

- Transportation

- Entertainment

- Insurance

- Savings

Read also:

Budgeting toolkit with Excel examples

2. Build an Emergency Fund

An emergency fund protects you against unexpected financial problems like:

- Job loss

- Medical emergencies

- Car repairs

- Unexpected bills

Most financial experts recommend saving between three and six months of living expenses.

Emergency Fund Formula

Emergency Fund = Monthly Expenses × Number of Months

Example

- Monthly expenses = $3,000

- Emergency target = 6 months

Emergency Fund = $3,000 × 6 = $18,000

This emergency reserve creates financial security and reduces dependence on credit cards or loans.

3. Debt Management

High-interest debt is one of the biggest financial problems for individuals.

Prioritize paying off:

- Credit card debt

- Personal loans

- High-interest financing

Always focus first on debts with the highest interest rates.

Debt Interest Formula

Interest = Loan Amount × Interest Rate

Example

- Credit card debt = $10,000

- Interest rate = 18%

Annual Interest = $10,000 × 18% = $1,800

Paying off high-interest debt quickly can save thousands of dollars.

Read also:

Wealth management guide

4. Set Saving Goals

Saving goals create motivation and financial direction.

Examples include:

- Vacation savings

- Buying a car

- Buying a house

- Retirement savings

- Education funds

- Business investment

Savings Goal Formula

Monthly Savings Needed = Goal Amount / Number of Months

Example

- Vacation budget = $6,000

- Timeframe = 12 months

Monthly Savings Needed = $6,000 / 12 = $500

Clear goals make saving easier and more disciplined.

Read also:

SMART goals and objectives

5. Learn About Investing

Investing helps money grow over time through compound growth.

Common investments include:

- Stocks

- Bonds

- Mutual funds

- ETFs

- Real estate

- Retirement accounts

Compound Interest Formula

Future Value = Present Value × (1 + Interest Rate)^Years

Investment Example

- Investment = $10,000

- Annual return = 8%

- Investment period = 10 years

Future Value = $10,000 × (1.08)^10 = $21,589

This shows how compound growth can significantly increase wealth over time.

6. Retirement Planning

The earlier you start saving for retirement, the more time your investments have to grow.

Financial advisors often recommend saving 10% to 15% of annual income for retirement.

Retirement Savings Formula

Annual Retirement Savings = Annual Income × Savings Rate

Example

- Annual income = $80,000

- Savings rate = 15%

Retirement Savings = $80,000 × 15% = $12,000 per year

Starting early reduces the pressure to save large amounts later.

7. Insurance Protection

Insurance protects your finances against major financial risks.

Important insurance types include:

- Health insurance

- Life insurance

- Disability insurance

- Home insurance

- Car insurance

Without insurance, a single emergency can destroy years of savings.

8. Avoid Impulse Purchases

Impulse spending destroys budgets and delays financial goals.

Before buying non-essential items:

- Wait 24 hours

- Compare prices

- Ask if the purchase is necessary

- Check your monthly budget first

Impulse Spending Example

- Impulse purchases per month = $300

Annual unnecessary spending = $300 × 12 = $3,600

Small unnecessary expenses become large financial losses over time.

9. Improve Financial Literacy

Financial literacy means understanding money management.

Learn about:

- Budgeting

- Investing

- Taxes

- Debt management

- Retirement planning

- Cash flow

- Risk management

The more financial knowledge you have, the better your financial decisions become.

10. Seek Professional Advice

Professional financial advisors can help create personalized strategies.

They can assist with:

- Investment planning

- Retirement planning

- Tax optimization

- Debt reduction

- Estate planning

- Budget optimization

Professional advice often helps people avoid expensive financial mistakes.

Common Personal Finance Mistakes

- Living beyond your income

- Not saving for emergencies

- Ignoring retirement planning

- Using too much credit card debt

- Making impulse purchases

- Not tracking expenses

- Investing without research

- Not having financial goals

- Ignoring insurance protection

- Depending only on one income source

Avoiding these mistakes significantly improves financial stability.

Best Financial Ratios for Personal Finance

Savings Ratio

Savings Ratio = Monthly Savings / Monthly Income × 100

Example

- Monthly savings = $1,000

- Monthly income = $5,000

Savings Ratio = ($1,000 / $5,000) × 100 = 20%

Debt-to-Income Ratio

Debt-to-Income Ratio = Monthly Debt Payments / Monthly Income × 100

Example

- Monthly debt payments = $1,200

- Monthly income = $5,000

Debt-to-Income Ratio = ($1,200 / $5,000) × 100 = 24%

Lower debt ratios improve financial flexibility.

Related Financial Resources

Need Help Managing Your Finances?

At Consultant4Companies, we help individuals and businesses improve budgeting, financial planning, investment analysis, cash flow management, and long-term financial strategies.